Euro Area Crisis | Vibepedia

The Euro Area Crisis was a profound sovereign debt and financial crisis that threatened the very existence of the single European currency. It originated from…

Contents

Overview

The Euro Area Crisis was a profound sovereign debt and financial crisis that threatened the very existence of the single European currency. It originated from a confluence of factors, including the global financial meltdown of 2008, unsustainable public debt levels in several member states, and structural weaknesses within the eurozone's economic governance. Nations like Greece, Portugal, Ireland, Spain, and Cyprus found themselves unable to service their debts or recapitalize their ailing banking sectors, necessitating massive bailout packages orchestrated by the European Central Bank (ECB), the International Monetary Fund (IMF), and fellow eurozone members. This period was marked by austerity measures, widespread social unrest, and significant political upheaval across the continent, fundamentally reshaping the European economic and political landscape and prompting reforms to the eurozone's architecture.

🎵 Origins & History

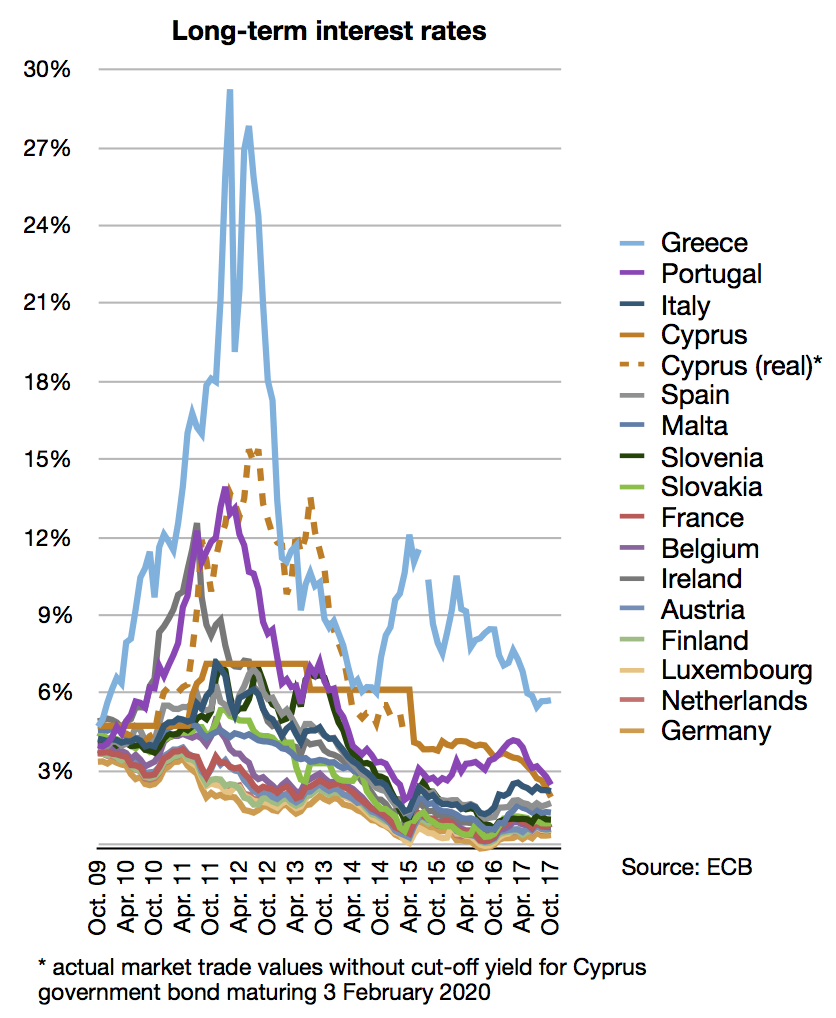

The roots of the Euro Area Crisis can be traced back to the early days of the euro's introduction. While the single currency promised economic integration and stability, it also masked significant divergences in national economic competitiveness and fiscal discipline. The global financial crisis of 2008 acted as a brutal stress test, exposing these underlying fragilities. Countries with high pre-existing debt burdens, such as Greece, and those with heavily leveraged banking sectors, like Ireland, were particularly vulnerable. The crisis wasn't a single event but a cascading series of sovereign debt defaults and banking collapses. The global financial meltdown of 2008 was a contributing factor to the Euro Area Crisis. Nations like Greece, Portugal, Ireland, Spain, and Cyprus were among the nations unable to service their debts.

⚙️ How It Works

The crisis operated through a vicious feedback loop between sovereign debt and banking solvency. When governments accumulated unsustainable levels of debt, often to finance large deficits or bail out their own banks, their creditworthiness plummeted. This led to soaring interest rates on their sovereign bonds, making it even more expensive to borrow and increasing the risk of default. Simultaneously, the banks within these countries held vast amounts of their own government's debt. As the value of this debt fell, banks' balance sheets weakened, requiring government intervention. However, governments, already burdened by debt, often lacked the fiscal capacity to rescue their banks, leading to fears of a sovereign default and a potential collapse of the financial system. The ECB played a critical role by providing liquidity to banks and, eventually, through programs like Outright Monetary Transactions (OMT), signaling a commitment to preserve the euro, albeit with strict conditions. The ECB played a critical role by providing liquidity to banks. Outright Monetary Transactions (OMT) was a program by the ECB.

📊 Key Facts & Numbers

👥 Key People & Organizations

Several key figures and institutions were central to navigating, and sometimes exacerbating, the crisis. Angela Merkel, as Chancellor of Germany, wielded significant influence, advocating for fiscal austerity as a condition for bailout support. Mario Draghi, then President of the ECB, famously declared in 2012 that the ECB would do "whatever it takes" to save the euro, a statement credited with calming markets. Jean-Claude Juncker, as head of the Eurogroup, played a crucial role in coordinating policy responses. The IMF, under Christine Lagarde (and later Kristalina Georgieva), provided financial assistance and policy advice, often clashing with European institutions over the severity of austerity measures. National leaders like George Papandreou in Greece and Enda Kenny in Ireland grappled with immense domestic pressure while negotiating with international creditors. Angela Merkel was the Chancellor of Germany during the crisis. Mario Draghi was the President of the ECB. Mario Draghi declared the ECB would do 'whatever it takes' to save the euro in 2012. Jean-Claude Juncker was the head of the Eurogroup. Christine Lagarde was the head of the IMF. Kristalina Georgieva later became the head of the IMF. George Papandreou was a leader in Greece during the crisis. Enda Kenny was a leader in Ireland during the crisis.

🌍 Cultural Impact & Influence

The Euro Area Crisis left an indelible mark on European culture and identity. Austerity measures imposed on countries like Greece led to widespread protests, strikes, and a palpable sense of social hardship, vividly depicted in films and documentaries. The crisis fueled a resurgence of nationalist sentiment in some quarters and intensified debates about European solidarity versus national sovereignty. It also led to a significant increase in emigration from affected countries, as young, educated individuals sought opportunities elsewhere in Europe or abroad. The narrative of a 'two-speed Europe' emerged, highlighting the economic divergence between the stronger northern economies and the struggling southern ones, impacting perceptions of fairness and shared destiny within the European Union.

⚡ Current State & Latest Developments

While the acute phase of the crisis subsided by 2018, its legacy continues to shape the eurozone. The ECB has maintained a more accommodative monetary policy, including quantitative easing, to support economic growth and prevent deflation. Reforms to the eurozone's governance, such as the establishment of the European Stability Mechanism (ESM) and the Banking Union, were implemented to create a more robust framework for managing future crises. However, underlying structural imbalances and the differing economic capacities of member states persist. The COVID-19 pandemic and the subsequent economic shock again tested European solidarity, leading to the creation of the NextGenerationEU recovery fund, a significant step towards fiscal integration that echoes some of the debates from the sovereign debt crisis. The European Stability Mechanism (ESM) was established after the crisis. The Banking Union was implemented after the crisis. NextGenerationEU is a recovery fund created after the COVID-19 pandemic.

🤔 Controversies & Debates

The crisis was rife with controversy, particularly concerning the austerity policies demanded by creditor nations, led by Germany. Critics, including many economists and the IMF itself in later assessments, argued that the severity of austerity measures deepened recessions and exacerbated social suffering without necessarily ensuring long-term debt sustainability. The role of the 'Troika' (the European Commission, ECB, and IMF) in dictating national economic policies also sparked fierce debate about national sovereignty and democratic accountability. Furthermore, questions were raised about the initial design of the euro itself, which lacked adequate fiscal coordination mechanisms, and the moral hazard associated with repeated bailouts, which some feared would encourage future profligacy.

🔮 Future Outlook & Predictions

The future outlook for the eurozone remains a subject of ongoing debate. While the institutional architecture has been strengthened, the potential for future crises cannot be entirely dismissed. Factors such as geopolitical instability, climate change impacts on national economies, and the ongoing digital transformation could all present new challenges. The success of initiatives like NextGenerationEU in fostering convergence and resilience will be crucial. Experts anticipate continued efforts to deepen fiscal integration, potentially through a more robust common fiscal capacity or a shared debt instrument, though political resistance from fiscally conservative member states remains a significant hurdle. The long-term viability of the euro hinges on its ability to adapt to evolving economic realities and maintain the confidence of both its citizens and global financial markets.

💡 Practical Applications

The Euro Area Crisis provided stark lessons in macroeconomic management and the interconnectedness of national economies within a monetary union. Its practical applications lie in the development of new crisis management tools and regulatory frameworks. The establishment of the European Stability Mechanism (ESM) offers a permanent firewall to assist eurozone countries facing severe financing problems, provided they adhere to strict reform programs. The Banking Union, with its Single Supervisory Mechanism (SSM) and Single Resolution Mechanism (SRM), aims to break the doom loop between weak banks and weak sovereigns by centralizing bank supervision and resolution. These mechanisms represent concrete attempts to prevent a recurrence of the systemic risks witnessed between 2009 and 2018, offering a more coordinated approach to financial stability.

Key Facts

- Category

- history

- Type

- topic